At this point, the “retail apocalypse” has proven to be a lingering myth. After all, the industry just finished a year with strong sales and in 2017, retail sales outpaced the growth in the U.S. GDP.

At this point, the “retail apocalypse” has proven to be a lingering myth. After all, the industry just finished a year with strong sales and in 2017, retail sales outpaced the growth in the U.S. GDP.

But 2018 didn’t end happily ever after for every retail brand. In spite of healthy overall holiday sales, some brands like J.Crew, Sears, Macy’s, and J.C. Penney announced plans to shutter hundreds of stores.

So, why do these headlines tell such disparate stories?

As many retailers reading right now can likely attest, the sector is shifting in seismic ways. Some brands are going bust while others are blossoming. That’s because, rather than undergoing an apocalypse, the industry is experiencing a renaissance.

The Harvard Business Review points out that retail has reinvented itself multiple times over the last couple of centuries. Railroads and the rise of cities spawned department stores, and later the invention of automobiles led to sprawling shopping malls, pushing the likes of Woolworths and Marshall Field’s into extinction. And a similar shift is happening now.

“Every 50 years or so, retailing undergoes this kind of disruption. Retailers relying on earlier formats either adapt or die out as the new ones pull volume from their stores and make the remaining volume less profitable.” —HBR

Luxury retailers and budget brands are seeing encouraging growth while stores in the middle are closing by the dozens. But what’s behind this bifurcation, and which brands are adapting well?

Socioeconomic realities: The dwindling middle class

As we explored in our last issue, modern shoppers are more empowered than ever; technology has put a wealth of product information and data in their immediate grasp. Shoppers are also more discerning—not just because they can be, but because the economic realities of the last decade have forced many consumers to be more conscious about how they spend their disposable dollars.

“The industry is showing weakness in some areas while demonstrating strength in others. This divergence is what we refer to as the great retail bifurcation, and we view the change as highly related to changing consumer economics.” —Deloitte Insights

According to data from Deloitte Insights, the last decade was rough on 80% of U.S. consumers. The lower 40% income group struggled to keep up with expenses while the middle 40% saw its income shrink. And while incomes stagnated or decreased, the costs for many necessities now gobble up a bigger portion of the average paycheck. For example, health care costs shot up 62% while food spiked 17%.

As a result, the retail industry is mirroring this shrink in the middle class. With fewer discretionary dollars, the competition between retail brands is fierce and the need to differentiate is stronger than ever.

Amazon eats up vanilla retail brands competing on “convenience”

When attempting to understand the “why” behind this divergence in retail, you can’t discount Amazon’s relentless growth. According to recent data from eMarketer, Amazon was predicted to close 49.1% of all ecommerce sales in 2018 and 5% of all retail sales.

With this growing loss in market share, big-box brands that previously competed on convenience in the mid-priced tier have lost many of their sales to Amazon. Three of these traditional retailers (Sears, Radio Shack, and Payless) accounted for 6,985 of the stores that closed down in 2017.

But the growth of online shopping (and the magnetic draw of Amazon Prime) is only part of the story here. When you scratch the surface, you’ll realize mid-tier retailers were already vulnerable because of their lack of differentiation and refusal to adapt. Sure, the age of Amazon has forced the industry to pay attention to ecommerce, but more brick-and-mortar stores are opening than closing and the majority of sales still happen in-person.

“…the stores that are swimming in a sea of sameness—mediocre service, over-distributed and uninspiring merchandise, one-size-fits-all marketing, look-alike sales promotions and relentlessly dull store environments—are getting crushed.”

—Steve Dennis, Retail Consultant and President of SageBerry Consulting

Two roads diverged: Premium versus discount brands

As a consequence of those increasingly tightened budgets and more discerning tastes, consumers are passing over middle-of-the-road retailers that provide mid-tier products and shopping experiences.

Instead, they’re opting for premium retailers peddling quality products and memorable experiences, or budget-conscious brands that offer economical shopping experiences with low prices to match.

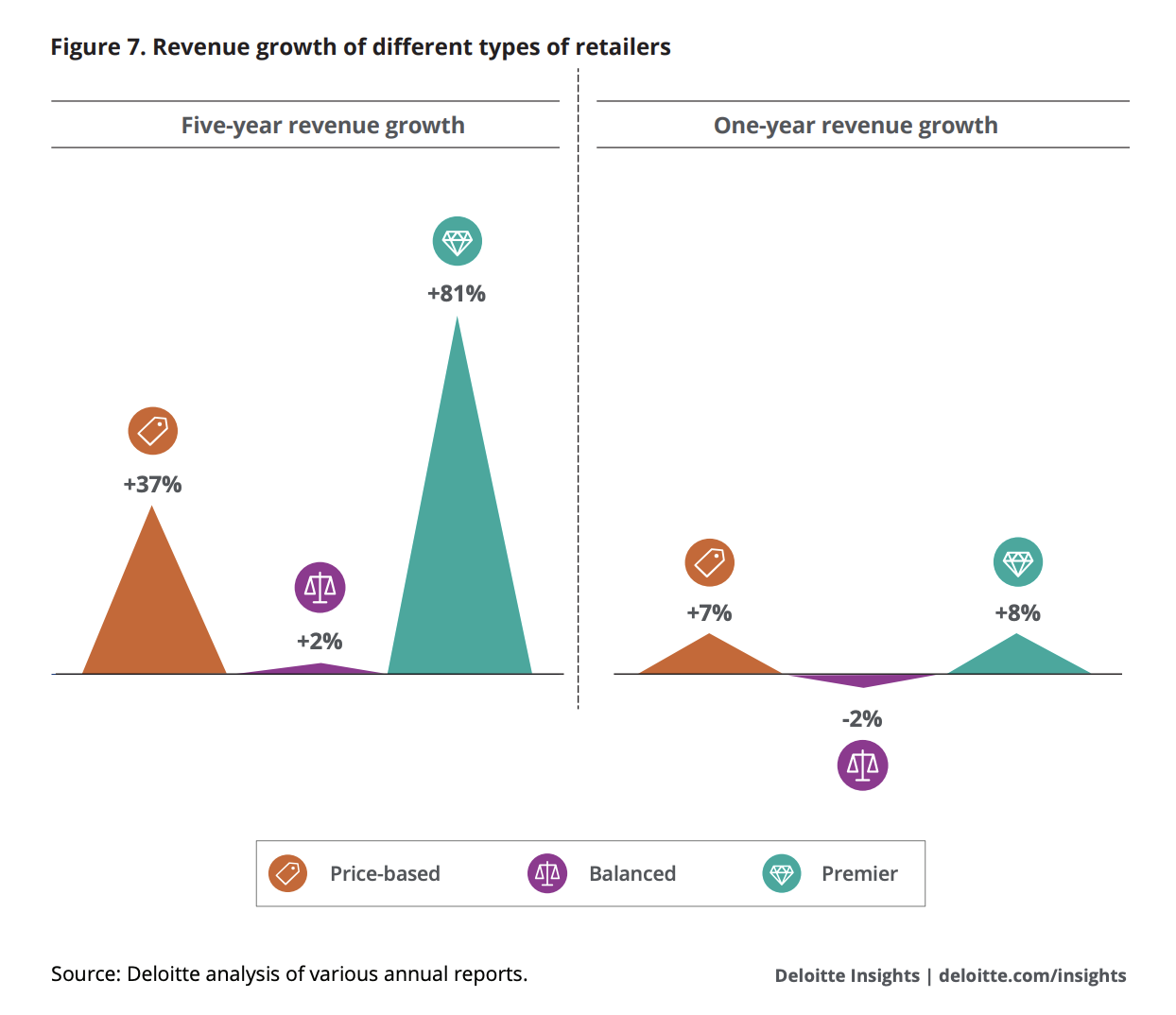

As illustrated in the chart below by Deloitte Insights, most of the growth is concentrated at the opposite ends of the spectrum—leaving brands in the middle to adapt or die off.

High-end brands, notably those with equally high-end experiences, saw their revenue grow 81%, or 40-times more than mid-tier retailers. Premium retailers that emphasize memorable in-store experiences are thriving (see Allbirds, AdoreMe, and The Sill, among many others).

On the other end of the spectrum, cost-conscious brands opened 2.5 new stores for every shop that balanced retailers opened and also saw their revenues spike by 37%. Drugstores, convenience stores, and dollar stores made up the top segments of retailers opening new locations. Off-price retailers are also seeing sales shoot up: Discount retail chain Ross saw a 7.8% revenue spike.

“Retailers should be mindful of these industry-wide trends. We see a divergence happening where consumers are choosing very low-priced items or premium items, with less consideration for products that fall in the middle.”

—Arpan Podduturi, Shopify’s Director of Product, Retail

Bridging the great divide

As this bifurcation continues to divide brands into two distinct categories, many retailers are staring down two divergent paths: competing on price or offering a premium experience.

While “value” stores serve a strong purpose (who doesn’t love bargain hunting?), high-touch experiences offer retailers a number of benefits. While online shopping is efficient, experience-driven retail’s hands-on, personalized experiences are ideal for shoppers who want something more than “click, cart, checkout.”

While this may not be the right path for every retailer, picking a lane and being deliberate about your strategy can help keep your retail brand out of the barren middle.

This was originally published as the first edition of the retail newsletter. To get industry updates and analysis delivered to your inbox, subscribe today.