This article is intended for those of you who are at the beginning of your investing journey and looking to gauge the potential return on investment in The Kroger Co (NYSE:KR).

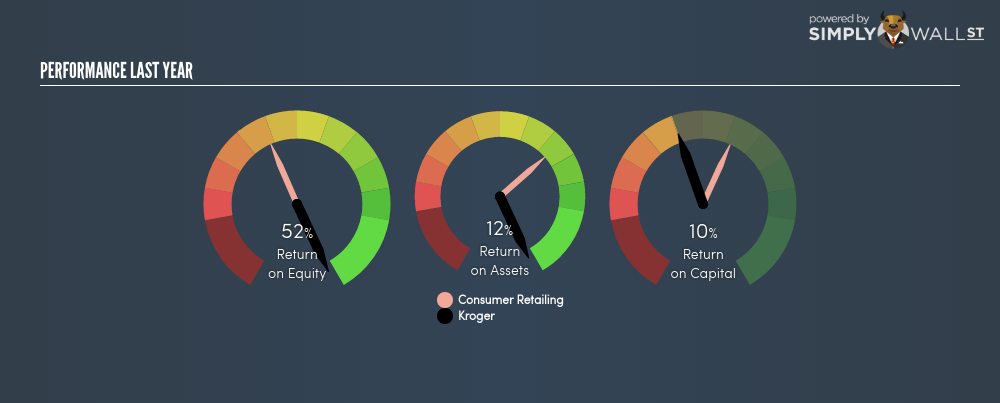

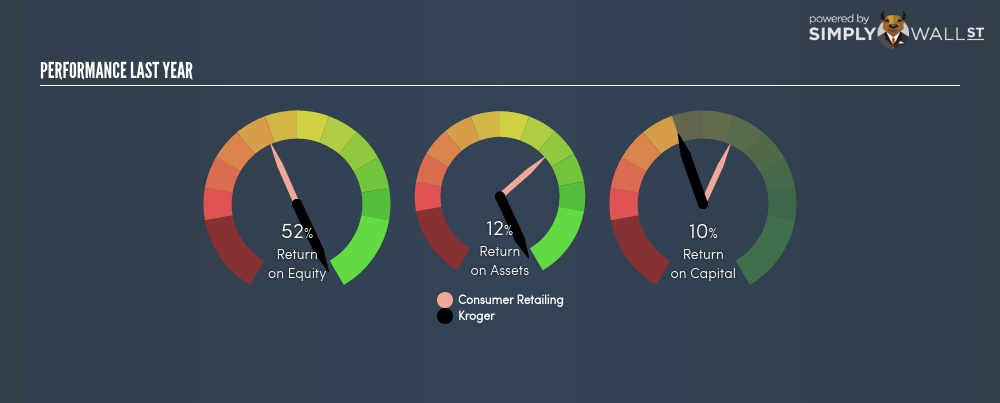

The Kroger Co (NYSE:KR) outperformed the food retail industry on the basis of its ROE – producing a higher 52.01% relative to the peer average of 12.22% over the past 12 months. But what is more interesting is whether KR can sustain this above-average ratio. Sustainability can be gauged by a company’s financial leverage – the more debt it has, the higher ROE is pumped up in the short term, at the expense of long term interest payment burden. Let me show you what I mean by this. View out our latest analysis for Kroger

Breaking down ROE — the mother of all ratios

Return on Equity (ROE) weighs Kroger’s profit against the level of its shareholders’ equity. It essentially shows how much the company can generate in earnings given the amount of equity it has raised. Investors seeking to maximise their return in the Food Retail industry may want to choose the highest returning stock. However, this can be misleading as each firm has different costs of equity and debt levels i.e. the more debt Kroger has, the higher ROE is pumped up in the short term, at the expense of long term interest payment burden.

Return on Equity = Net Profit ÷ Shareholders Equity

ROE is assessed against cost of equity, which is measured using the Capital Asset Pricing Model (CAPM) – but let’s not dive into the details of that today. For now, let’s just look at the cost of equity number for Kroger, which is 8.59%. This means Kroger returns enough to cover its own cost of equity, with a buffer of 43.42%. This sustainable practice implies that the company pays less for its capital than what it generates in return. ROE can be broken down into three different ratios: net profit margin, asset turnover, and financial leverage. This is called the Dupont Formula:

Dupont Formula

ROE = profit margin × asset turnover × financial leverage

ROE = (annual net profit ÷ sales) × (sales ÷ assets) × (assets ÷ shareholders’ equity)

ROE = annual net profit ÷ shareholders’ equity

NYSE:KR Last Perf June 29th 18

NYSE:KR Last Perf June 29th 18

The first component is profit margin, which measures how much of sales is retained after the company pays for all its expenses. The other component, asset turnover, illustrates how much revenue Kroger can make from its asset base. The most interesting ratio, and reflective of sustainability of its ROE, is financial leverage. We can assess whether Kroger is fuelling ROE by excessively raising debt. Ideally, Kroger should have a balanced capital structure, which we can check by looking at the historic debt-to-equity ratio of the company. The most recent ratio is 206.04%, which is relatively high, indicating Kroger’s above-average ROE is generated by its high leverage and its ability to grow profit hinges on a sizeable debt burden.

NYSE:KR Historical Debt June 29th 18

NYSE:KR Historical Debt June 29th 18

Next Steps:

While ROE is a relatively simple calculation, it can be broken down into different ratios, each telling a different story about the strengths and weaknesses of a company. Kroger’s above-industry ROE is encouraging, and is also in excess of its cost of equity. Its high debt level means its strong ROE may be driven by debt funding which raises concerns over the sustainability of Kroger’s returns. Although ROE can be a useful metric, it is only a small part of diligent research.

For Kroger, there are three important factors you should further examine:

- Financial Health: Does it have a healthy balance sheet? Take a look at our free balance sheet analysis with six simple checks on key factors like leverage and risk.

- Valuation: What is Kroger worth today? Is the stock undervalued, even when its growth outlook is factored into its intrinsic value? The intrinsic value infographic in our free research report helps visualize whether Kroger is currently mispriced by the market.

- Other High-Growth Alternatives : Are there other high-growth stocks you could be holding instead of Kroger? Explore our interactive list of stocks with large growth potential to get an idea of what else is out there you may be missing!

TOP undervalued stocks for 2017

Looking for undervalued stocks? The trick is not to follow the herd. These overlooked companies are now trading for less than their intrinsic value. Click here to see them for FREE on the Simply Wall St platform.